A few years back in 2012, a new card network was launched in India as an alternative to Visa and MasterCard. It was named RuPay, which sounds like a combination of Indian currency 'Rupee' and the verb 'to pay'. Within just ten years, it became the biggest competitor in the Indian card market and captured 60% of the whole market share in 2020. It became such a severe threat that Visa complained about the dominance of RuPay to the US Government.

In 2022, when a majority of the population is using RuPay, completely dominating over Visa and MasterCard, a curiosity arises about the whole process. How did RuPay become so powerful in just a few years? The current article tries to discuss the same.

Situation Before RuPay

Visa and MasterCard were dominating in the Indian card markets before RuPay. However, they were only concerned with a small percentage of the Indian population, the upper class. Only 55 banks in India were supported by these companies, most of which were corporate or private banks. Until recently, the majority of India's population was unaware of such amenities, and even if they were, they couldn't afford them.

RBI had mentioned in its 2009-12 vision paper about India Card - A domestic card initiative. Then NPCI took over from that, renamed it RuPay, and started working on a domestic payment card that would act as an alternative for MasterCard and Visa. RuPay was launched in March 2012 for public usage.

Before Diving Deep

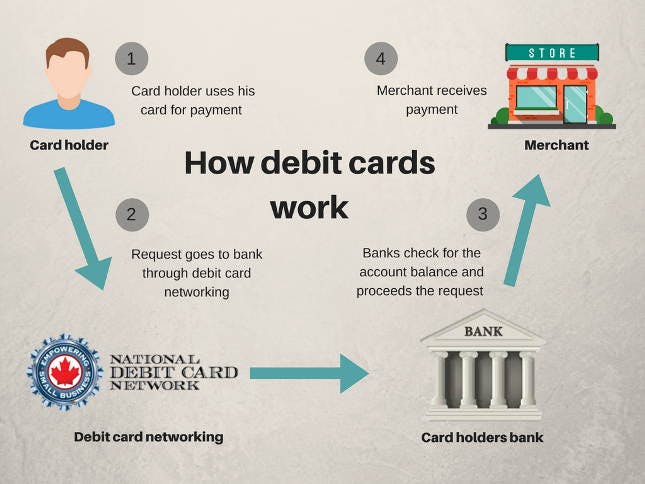

Before diving deep, let's understand a few terms and the working of a traditional card payment system. When you swipe a card in the EPOS system, many things happen in the background, and many parties participate in the process.

Involved Parties

Three main parties that take part in the transaction are:

- Issuing Bank: The bank where the customer has their account. It issues debit cards to its users and holds their funds.

- Acquiring Bank: The bank that acquires funds at the end of the transaction. It is the bank where merchants have their accounts.

- Card Networks: The card network company acts as an essential intermediary between the whole transaction. The big bulls in the business are VISA, MasterCard and RuPay.

Transaction Process

The transaction starts when the customer enters the correct password. Then the card network takes charge of the process, which can be summarized in three steps:

- Authorization: The card company checks the status of the customer's account. If it is not blocked, empty or suspicious, authorization is considered successful.

- Capture: Funds are captured from the customer's bank account, and the merchant is notified through the EPOS system. The deal between customer and merchant is considered done here, but the acquiring bank still has not received funds.

- Settlement: Settlement is the process of transferring money from an issuing bank account to an acquiring bank account. Settlement usually occurs once in a business day. At the end of the process, the merchant finally receives the money.

Merchant Discount Rate

However, there is a catch. The merchant does not receive the total amount sent by the customer. During the payment, involved parties take a few percentages. This fee is known as the Merchant Discount Rate or MDR. MDR is to blame if you are refused card payments in small businesses. MDR is determined by the type of card used. A debit card is charged 0.9%, and a credit card is charged anywhere from 1% to 3% of the total amount.

If a payment gateway like Stripe, Bill desk, or Razorpay is involved, it charges a small percentage. This charge is called a Payment Service Provider Fee, usually 0.5% of the overall amount.

Simply put, when a customer buys something for 10,000 and pays with a card, the merchant will only receive 9,650 rupees.

Implementation of RuPay

Indian Government and NPCI saw major gaps in this system. The system was not wholly flawed but had major drawbacks and areas of improvement.

- A large population of India works in an uncategorized sector. They are daily wagers, day to day workers and vendors. Most of them can't even afford a bank account for multiple reasons: minimum balance constraint, complexity in the process of withdrawals and credit, to name a few. As per a report, a total of 557 million Indian population was unbanked in 2011.

- Even though VISA and MasterCard have a duopoly in card payments, they were partnered with only 55 banks in India. Most of them are private or corporate banks. There was no support for other banks whatsoever.

NPCI leveraged these disadvantages and started working precisely on them. NPCI, RBI and the Indian government started zero-balance bank accounts for people who can't afford to put much money in banks. Until 2015, the Indian unbanked population was halved to 223million compared to 2011. People from the bottom of the pyramid were getting into finance and banking and benefiting from it.

Visa and MasterCard have international networks but Most RuPay customers transacted within India, so rupay was initially India's only cheaper option which later expanded its service with time

RuPay's MDR Policy

When RuPay was launched, it had a fixed MDR of 90 Indian paise regardless of the amount to be transacted. It was a huge factor considering how much Visa and MasterCard used to charge. It became possible for everyone to accept card-based payments. A few years back, in late 2019, the finance minister announced the Zero-MDR policy for RuPay. That means no extra charge will be deducted from the transaction. Since then, More merchants have been encouraged to use it along with the existing UPI system with a Zero-MDR policy.

Contribution of Indian Government

The Indian government itself promotes RuPay. The government successfully encouraged the Indian population to have an active bank account through RuPay and other government schemes. This laid the groundwork for Indian citizens' financial inclusion and created a pipeline for the government to efficiently distribute schemes and services to people who would otherwise have had such opportunities.

In just a few years, NPCI announced four more cards under RuPay.

- PMJDY Debit Card: It gives you instant access to your bank account anywhere from India. And it has personal accident death protection and disability coverage for the customer.

- Mudra Card: A customer can perform multiple withdrawals and credits to cost-effectively manage the working capital limit.

- PunGrain Card: It offers a cash withdrawal facility, and its transaction cost is also meagre. It was exclusively designed for farmers having a particular account.

- Kisan Card: Again focusing on the farmers, the Kisan card is a need-based timely credit system.

What Lies Next

After being the largest in Indian markets, RuPay is now expanding internationally. RuPay entered global markets in 2014 itself. According to a report, RuPay has issued over 64 million cards until 2019. These cards are accepted by 1.8 million ATMs and 41 million merchants in 190 countries around the globe. Singapore, UAE and Japan are a few countries showing massive interest in adapting RuPay.

Despite all of this, RuPay has not shown its presence in a few other markets. Even though it has acquired the most significant share in the Indian debit card market, it still falls far behind in the credit card market. It holds only around 20% of the Indian market, and Visa and MasterCard dominate credit cards.

Farewell

I came across this topic while researching the digital payment revolution in India for my article last month and became immediately interested in learning more. Let me know if you found this interesting or have any suggestions or improvements. I am most active on Twitter, LinkedIn, and Showcase. I also maintain a personal blog where I talk about web development, programming and general experience.

Happy swiping!